So why the title of this blog?

Our modern financial system is based on paper currencies, which have no intrinsic value. The 100 USD note has value because we can exchange it for goods and services, but also and more importantly, because there is is a limited supply of 100 USD notes in the world, and (even more importantly), because we trust that that supply will not go up too fast.

The truth is however, that over time, with the rising supply of money, cash has indeed lost quite a bit of their value in real terms. This charts shows the decline in value of one (nominal) USD using the consumer price index:

With the Fed's target of "low but positive inflation" a dollar has turned into 6 cents. Another aspect of the Fed's policy that contributed to this decline, is its willingness to intervene (ie print or lend money) in times of crisis. This was taken to an extreme during the Greenspan era, when every significant decline in stock prices was met with more expansionary monetary policy. After the initial shock, this liquidity is usually not withdrawn, and the money supply (and debt) ends up increasing faster than economic activity.

With the Fed's target of "low but positive inflation" a dollar has turned into 6 cents. Another aspect of the Fed's policy that contributed to this decline, is its willingness to intervene (ie print or lend money) in times of crisis. This was taken to an extreme during the Greenspan era, when every significant decline in stock prices was met with more expansionary monetary policy. After the initial shock, this liquidity is usually not withdrawn, and the money supply (and debt) ends up increasing faster than economic activity.So the unit we use for measuring value, and often as a store of wealth, is actually an asset with ever less real value, as its quantity can be easily changed by the authorities, in order to accommodate short-term objectives. This phenomenon was not confined to the US Dollar, most countries have maintained positive inflation, and effectively been devaluing their currencies in real terms.

All this is relevant today, because the developed world is facing the most dismal economic outlook:

1) debt and future liabilities are way too high

and

2) many tail winds from the past years are turning into head winds

...and chances are very high, in my opinion, that the most convenient way for authorities to get through this, will be to print, and make the loss of wealth and income less obvious in nominal terms. As John Maynard Keynes famously said about inflation: There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.

Debt and Future Liabilities

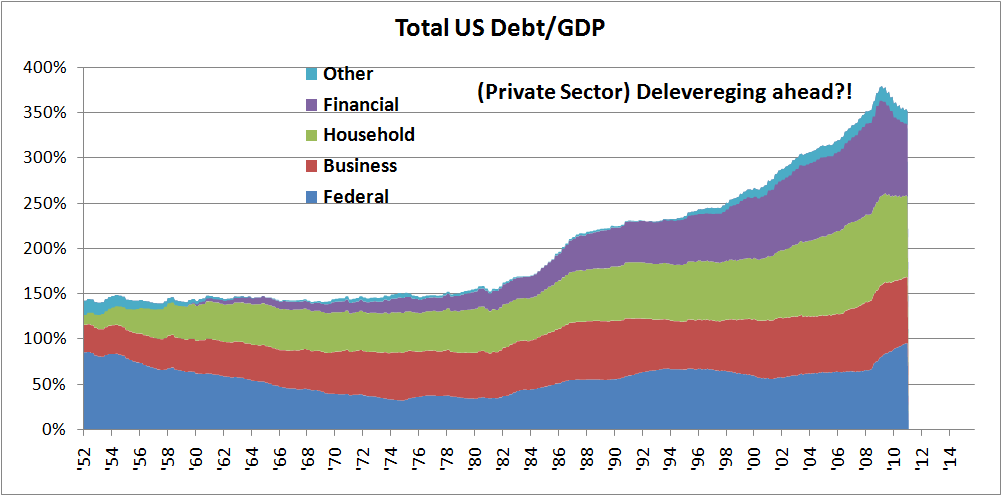

During the last 30 years debt levels have exploded in the US. Most of this debt build up occurred at the consumer (or household) level, with many people borrowing against real estate, but the financial system also became more highly leveraged. On my latest numbers this brings the total to 336% of GDP, with household debt at 89% and government debt at 95%.

With the financial crises, and collapse in real estate values, the private sector has stopped borrowing more, and in order to avoid a prolonged recession or depression the government stepped in, increasing government spending and deficits:

With the financial crises, and collapse in real estate values, the private sector has stopped borrowing more, and in order to avoid a prolonged recession or depression the government stepped in, increasing government spending and deficits: We are now at a juncture where the government is running unsustainable fiscal deficits of 10% in order to maintain growth at a reasonable level, while the private sector heals. However, so far it is difficult to speak of any improvement at the private sector level, rather a stabilization at best. It should also be noted, that the fiscal deficit can only be reduced gradually (say 2-3 percentage points/year) without bringing the economy down.

We are now at a juncture where the government is running unsustainable fiscal deficits of 10% in order to maintain growth at a reasonable level, while the private sector heals. However, so far it is difficult to speak of any improvement at the private sector level, rather a stabilization at best. It should also be noted, that the fiscal deficit can only be reduced gradually (say 2-3 percentage points/year) without bringing the economy down.The public debt situation level is high as it is, however it gets worse. Demographics - the retirement of baby boomers - and promises made by the US government imply and significant rise in government spending on social security and health in the coming years.

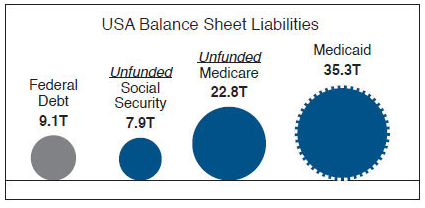

This graph was taken from the Pimco website, from a recent monthly piece by Bill Gross. It shows the massive unfunded obligations of the US government related to socail security and health (this category is otherwise known as entitlement spending). As a side note, the US government has 14.27 trillion USD of debt (the number I use in the total debt chart), however Bill Gross uses the category called debt held by public for the smallest circle, which excludes ~5tn of debt held in government accounts for funding future social security spending and the like. BTW neither includes Freddie Mac and Fannie Mae debt at a cool 40%+. The big blue circles are future entitlement obligations, and they dwarf existing public debt.

This graph was taken from the Pimco website, from a recent monthly piece by Bill Gross. It shows the massive unfunded obligations of the US government related to socail security and health (this category is otherwise known as entitlement spending). As a side note, the US government has 14.27 trillion USD of debt (the number I use in the total debt chart), however Bill Gross uses the category called debt held by public for the smallest circle, which excludes ~5tn of debt held in government accounts for funding future social security spending and the like. BTW neither includes Freddie Mac and Fannie Mae debt at a cool 40%+. The big blue circles are future entitlement obligations, and they dwarf existing public debt.The debate in Washington, about the debt ceiling and budget reform does not make one optimistic, and appears like mostly posturing by the republicans. What is clear from this, is that entitlement reform (ie reduction) is what is needed to avoid disaster, but it is also a very unpopular political decision nobody wants to make. Today "entitlements" represent 55% of the budget outlays, defense is 20% and interest payments are 6%. Most of the haggling between the two parties is concentrated on the remaining 19% (the nondefense discretionary category), which covers such trivialities as education, police, highways - ie all other government spending.

Although the outlook for the US is particularly poor, most developed countries are facing similar challenges. Even if debt growth was not as extravagant in the last two decades in, say, France, the problem of unfunded pension and health spending, with a deteriorating demographic ratio is certainly real and comparable. Indeed, the seven (most) industrialized nations are on a terrible debt trajectory:

Even Germany, the bastion of fiscal responsibility and the European leader in manufacturing and exports, doesn't look good:

Even Germany, the bastion of fiscal responsibility and the European leader in manufacturing and exports, doesn't look good: It should be noted, that Emerging Markets are not faced with that kind of debt overhang, and thus have much better prospects:

It should be noted, that Emerging Markets are not faced with that kind of debt overhang, and thus have much better prospects:

Structural Winds of Change

As noted earlier, debt has been rising very fast for the last quarter century, nicely outpacing GDP growth. This was a strong growth tailwind as can be seen here:

The Credit Impulse is the change in the rate of growth of credit (in this case household+corporate debt). It has provided a boost to GDP for the bigger part of the past three decades. It is safe to say that debt can not keep on growing at this pace, as debt levels are already at unprecedented and dangerous levels. Going forward debt dynamics will be a headwind.

The Credit Impulse is the change in the rate of growth of credit (in this case household+corporate debt). It has provided a boost to GDP for the bigger part of the past three decades. It is safe to say that debt can not keep on growing at this pace, as debt levels are already at unprecedented and dangerous levels. Going forward debt dynamics will be a headwind.

Interest rates have been trending down since early 80's (when Paul Volcker squeezed the pips out of inflation)

This phenomenon had massively positive implications for the value of assets (bonds up, equities up, real estate up - all seem more attractive and profitable as cost of financing goes down) and leverage (can borrow more). This phenomenon was driven by other very important trends such as:

This phenomenon had massively positive implications for the value of assets (bonds up, equities up, real estate up - all seem more attractive and profitable as cost of financing goes down) and leverage (can borrow more). This phenomenon was driven by other very important trends such as:

1) global disinflation as Asia becomes the (cheap) supplier of many tradable goods and

2) as Asian (and other EM) currencies are pegged to the USD and run trade surpluses, these countries accumulate USD reserves and "recycle" or reinvest them in US treasuries, thus making financing for US entities cheaper.

There is good reasons to believe that all of these are slowly changing course. Asia no longer provides an unlimited pool of cheap labor, and there has been a lot of anecdotal evidence in the past year of rising wages and even labor shortage in China, as well as stories of rapid rises in salaries for low-skilled workers elsewhere in Asia (ie in Bangladesh from 40 to 80 USD/month for textile workers).

Currency revaluation pressures (generally through the inflationary mechanism) are putting pressure on many EM currencies to appreciate, which will bring the current accounts closer to balance and reserve accumulation will slow if not stop. Global reserves held at Central Banks have reached 9.86 trillion USD, and appetite for further accumulation, and more importantly accumulation of US bonds is not there. China realizes that it already holds way too much US debt.

A trade-off, which is getting worse, is the one between growth and inflation. Apart from wage pressures in low-cost countries, we are also confronted with an increasing competition for finite resources. Emerging Countries, who represent a much larger population than developed countries (very roughly 4bn people vs <1bn in developed) are growing and consuming an ever larger share of energy, metals and food stuffs, which puts pressure on prices.

In the past, only after several quarters of very strong growth, would commodity prices start to rise. This time around we had the slowest recovery from a recession (in the West), and the highest rise in commodity prices (post-recession). This is something we unfortunately have to get used to, as the resources EM is competing for, are finite and ever more costly to extract.

In the past, only after several quarters of very strong growth, would commodity prices start to rise. This time around we had the slowest recovery from a recession (in the West), and the highest rise in commodity prices (post-recession). This is something we unfortunately have to get used to, as the resources EM is competing for, are finite and ever more costly to extract.

It should be remembered, that the US is the biggest consumer of oil in the world (18.7mbpd out of 82.8mbpd) and two-thirds are imported.

It should be remembered, that the US is the biggest consumer of oil in the world (18.7mbpd out of 82.8mbpd) and two-thirds are imported.

The Credit Impulse is the change in the rate of growth of credit (in this case household+corporate debt). It has provided a boost to GDP for the bigger part of the past three decades. It is safe to say that debt can not keep on growing at this pace, as debt levels are already at unprecedented and dangerous levels. Going forward debt dynamics will be a headwind.

The Credit Impulse is the change in the rate of growth of credit (in this case household+corporate debt). It has provided a boost to GDP for the bigger part of the past three decades. It is safe to say that debt can not keep on growing at this pace, as debt levels are already at unprecedented and dangerous levels. Going forward debt dynamics will be a headwind.Interest rates have been trending down since early 80's (when Paul Volcker squeezed the pips out of inflation)

This phenomenon had massively positive implications for the value of assets (bonds up, equities up, real estate up - all seem more attractive and profitable as cost of financing goes down) and leverage (can borrow more). This phenomenon was driven by other very important trends such as:

This phenomenon had massively positive implications for the value of assets (bonds up, equities up, real estate up - all seem more attractive and profitable as cost of financing goes down) and leverage (can borrow more). This phenomenon was driven by other very important trends such as:1) global disinflation as Asia becomes the (cheap) supplier of many tradable goods and

2) as Asian (and other EM) currencies are pegged to the USD and run trade surpluses, these countries accumulate USD reserves and "recycle" or reinvest them in US treasuries, thus making financing for US entities cheaper.

There is good reasons to believe that all of these are slowly changing course. Asia no longer provides an unlimited pool of cheap labor, and there has been a lot of anecdotal evidence in the past year of rising wages and even labor shortage in China, as well as stories of rapid rises in salaries for low-skilled workers elsewhere in Asia (ie in Bangladesh from 40 to 80 USD/month for textile workers).

Currency revaluation pressures (generally through the inflationary mechanism) are putting pressure on many EM currencies to appreciate, which will bring the current accounts closer to balance and reserve accumulation will slow if not stop. Global reserves held at Central Banks have reached 9.86 trillion USD, and appetite for further accumulation, and more importantly accumulation of US bonds is not there. China realizes that it already holds way too much US debt.

A trade-off, which is getting worse, is the one between growth and inflation. Apart from wage pressures in low-cost countries, we are also confronted with an increasing competition for finite resources. Emerging Countries, who represent a much larger population than developed countries (very roughly 4bn people vs <1bn in developed) are growing and consuming an ever larger share of energy, metals and food stuffs, which puts pressure on prices.

In the past, only after several quarters of very strong growth, would commodity prices start to rise. This time around we had the slowest recovery from a recession (in the West), and the highest rise in commodity prices (post-recession). This is something we unfortunately have to get used to, as the resources EM is competing for, are finite and ever more costly to extract.

In the past, only after several quarters of very strong growth, would commodity prices start to rise. This time around we had the slowest recovery from a recession (in the West), and the highest rise in commodity prices (post-recession). This is something we unfortunately have to get used to, as the resources EM is competing for, are finite and ever more costly to extract. It should be remembered, that the US is the biggest consumer of oil in the world (18.7mbpd out of 82.8mbpd) and two-thirds are imported.

It should be remembered, that the US is the biggest consumer of oil in the world (18.7mbpd out of 82.8mbpd) and two-thirds are imported.Conclusion and Implications

The above is to illustrate that the favorable growth dynamics of recent years and decades, are becoming much more unfavorable, while the developed countries (with very few exceptions), are confronted with a pile of debt and pension obligations to populations with ever more retirees. In short, I don't believe there is any way these liabilities can be made good in real terms. Thus it is only a question of how the governments will default on them. Inflation will most certainly play a role. Longer-term real return on government bonds should be very poor - not only is the starting nominal yield historically low, inflation over the next 10-20 years is likely to be above average.

The investment implications are:

- high economic volatility as cycles are shorter, as we oscillate between deflation to inflation

- this leads to higher financial market volatility - careful with leverage

- gold, the ultimate currency which can not be printed. Out of the 10 trillion of (EM) central bank reserves very little is held in gold, while over two-thirds are in USDs. Room to grow here as debasement worries rise.

- commodity producers - you want to own the companies who own the stuff in the ground... but it's cyclical and cycles will be vicious

- EM currencies (especially Asia+LatAM) - vs underweight in USD+EUR+JPY in particular

- EM stocks - of course a lot of micro-level factors play a role, but despite the recent hype, developed market investors have low allocations to this superior category

- as things get worse capital controls and various forms of financial repression will be enacted in developed countries, so careful where you hold your assets

Finally, it should be noted that this is not a cyclical call. We may very well have another deflationary scare ahead of us where US Treasuries rally, and hard assets underperform. The growth path of some still export-dependent EM will not be smooth. But ultimately, the authorities will "engage all the hidden forces of economic law" and produce inflation, which is their only chance to tackle the massive debt overhang.

The above is to illustrate that the favorable growth dynamics of recent years and decades, are becoming much more unfavorable, while the developed countries (with very few exceptions), are confronted with a pile of debt and pension obligations to populations with ever more retirees. In short, I don't believe there is any way these liabilities can be made good in real terms. Thus it is only a question of how the governments will default on them. Inflation will most certainly play a role. Longer-term real return on government bonds should be very poor - not only is the starting nominal yield historically low, inflation over the next 10-20 years is likely to be above average.

The investment implications are:

- high economic volatility as cycles are shorter, as we oscillate between deflation to inflation

- this leads to higher financial market volatility - careful with leverage

- gold, the ultimate currency which can not be printed. Out of the 10 trillion of (EM) central bank reserves very little is held in gold, while over two-thirds are in USDs. Room to grow here as debasement worries rise.

- commodity producers - you want to own the companies who own the stuff in the ground... but it's cyclical and cycles will be vicious

- EM currencies (especially Asia+LatAM) - vs underweight in USD+EUR+JPY in particular

- EM stocks - of course a lot of micro-level factors play a role, but despite the recent hype, developed market investors have low allocations to this superior category

- as things get worse capital controls and various forms of financial repression will be enacted in developed countries, so careful where you hold your assets

Finally, it should be noted that this is not a cyclical call. We may very well have another deflationary scare ahead of us where US Treasuries rally, and hard assets underperform. The growth path of some still export-dependent EM will not be smooth. But ultimately, the authorities will "engage all the hidden forces of economic law" and produce inflation, which is their only chance to tackle the massive debt overhang.

1 comment:

The recent comments from the Fed could be validating the inflationary approach:

*FED OFFICIALS SAID TO DISCUSS ADOPTING EXPLICIT INFLATION GOAL

*FED DISCUSSIONS OF INFLATION TARGET SAID TO BE ACTIVE, SERIOUS

Post a Comment